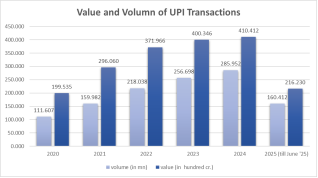

In 2016, the Indian government took a very firm stance on the black money market, which was followed by demonetization. Afterward, the government realized that the economy would benefit more from digital transactions and plastic money, considering Singapore as a reference. People were struggling to meet their basic needs; consequently, the government understood the importance of stabilizing the money supply, leading to the emergence of digital transactions and UPI. Objective: to investigate the dynamics of UPI transactions post-2020 and how UPI has been very critical in making financial inclusion a possibility in the Indian scenario. The paper also evaluates the role of UPI in MSMEs growth and development. Methods: Information about UPI transactions, including their volume and value, the number of active users, and their geographic distribution, was gathered using the NPCI dataset, on which we ran a linear regression model. For MSMEs, we saw a span of the last 4 years through the government’s annual report. Findings: Linear regression showed time predicts UPI transaction volume (R² = 0.97, p < 0.001) and value (R² = 0.837, p < 0.001), indicating that UPI adoption growth explains much of the rise in digital activity. The compound annual growth rate of UPI transaction value was about 19.75% from 2020 to 2024. The MSME transaction data from 2020-21 to 2023-24 shows a trend of an increase in the number and value of transactions, with the vast majority of them being carried out online during this time.

| Published in | International Journal of Economics, Finance and Management Sciences (Volume 13, Issue 5) |

| DOI | 10.11648/j.ijefm.20251305.19 |

| Page(s) | 336-344 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2025. Published by Science Publishing Group |

Unified Payment Interface, MSME, Digital Transaction, Economic Growth, Financial Inclusion

Source | SS | df | MS | Number of obs | 66 | |

|---|---|---|---|---|---|---|

Model | 23234.5515 | 1 | 23234.5515 | F(1,64) | 2071.19 | |

Residual | 717.94854 | 64 | 11.2179459 | Prob > F | 0.0000 | |

Total | 23952.5 | 65 | 368.5 | R-squared | 0.97 | |

| Adj R-Squared | 0.9696 | ||||

Root MSE | 3.3493 | |||||

month | Coef. | Std. Err. | t | P > |t| | [95% Conf. Interval] | |

perbank | 3.176047 | 0.0697873 | 45.51 | 0.000 | 3.036631 | 3.315464 |

_cons | -23.89451 | 1.326807 | -18.01 | 0.000 | -26.54512 | -21.24391 |

Source | SS | df | MS |

| Number of obs | 66 |

|---|---|---|---|---|---|---|

Model | 20051.8771 | 1 | 20051.8771 | F(1,64) | 329 | |

Residual | 3900.62288 | 64 | 60.9472325 | Prob > F | 0.0000 | |

Total | 23952.5 | 65 | 368.5 | R-squared | 0.8372 | |

| Adj R-Squared | 0.8346 | ||||

Root MSE | 7.8069 | |||||

month | Coef. | Std. Err. | t | P > |t| | [95% Conf. Interval] | |

perbankvalue | 0.0248299 | 0.0013689 | 18.14 | 0.000 | 0.0220952 | 0.0275646 |

_cons | -37.775 | 4.04529 | -9.34 | 0.000 | -45.85639 | -29.6936 |

Years | Total | By Digital Means | Percentages | |||

|---|---|---|---|---|---|---|

No. of transactions | Value in Rupees (In crore) | No. of transactions | Value in Rupees (In crore) | No. of Digital Transactions (in %) | Value of Digital Transactions (in %) | |

2020-21 | 3861529 | 18284.67 | 3376621 | 17946.58 | 90.19 | 92.02 |

2021-22 | 4135997 | 27292.98 | 3611362 | 26891.22 | 87.32 | 98.53 |

2022-23 | 5758260 | 20595.27 | 5104276 | 20115.15 | 88.64 | 97.67 |

2023-24 | 16620118 | 98,396.45 | 14486733 | 84046.984 | 87.16 | 85.42 |

AML | Anti-money Laundering |

BHIM | Bharat Interface for Money |

CAGR | Compound Annual Growth Rate |

DOI | Digital Object Identifier |

GDP | Gross Domestic Product |

IMPS | Immediate Payment Service |

MSME | Micro, Small, and Medium Enterprises |

NPCI | National Payments Corporation of India |

P2M | Person-to-Merchant |

P2P | Peer-to-peer |

PMJDY | Pradhan Mantri Jan Dhan Yojana |

RBI | Reserve Bank of India |

UPI | Unified Payment Interface |

| [1] | NITI Aayog. (2021). Digital payments: Trends, issues, and opportunities. Government of India. |

| [2] | Neema, K., & Neema, A. (2016). UPI (Unified Payment Interface) - A new technique of Digital Payment: An Explorative study. |

| [3] | Shree, S., Pratap, B., Saroy, R. et al. Digital payments and consumer experience in India: a survey based empirical study. J BANK FINANC TECHNOL 5, 1-20 (2021). |

| [4] |

Nisha. (2021). Technology and Financial Inclusion: An Agenda for Holistic Growth. International Journal of Management Studies (IJMS), 5(2(2), 35-39. Retrieved from

https://researchersworld.com/index.php/ijms/article/view/1752 |

| [5] | Mahajan, P., & Agarwal, M. (2023). Digital Payments and MSMEs: Assessing Potential and impact. IRJEMS International Research Journal of Economics and Management Studies, 549-553. |

| [6] | JishaJoseph, M., & Varghese, T. (2014). Role of financial inclusion in the development of Indian Economy. Growth, 5(11). |

| [7] | Karmakar, A. (2024). Unified Payments Interface (UPI): A Comprehensive Study of its Impact on India's Financial Landscape and Global Aspirations. |

| [8] | RBI Bank Blog. UPI payment - features and benefits of UPI payments. 2023 May 15. |

| [9] | Mehta, P., The Rise of Fintech in India: How Banks Manage Risk in the Digital Age (August 06, 2024). Available at SSRN: |

| [10] | Fahad, N., & Shahid, M. (2022). Exploring the determinants of adoption of Unified Payment Interface (UPI) in India: A study based on diffusion of innovation theory. Digital Business, 2(2), 100040. |

| [11] | Chaterji, A., Dr. Abhijeet, & Thomas, R. (2017). Unified Payment Interface (UPI): A Catalyst Tool Supporting Digitalization - Utility, Prospects & Issues. International Journal of Innovative Research and Advanced Studies (IJIRAS), 4(2). Available at SSRN: |

| [12] | Duvendack, M., Sonne, L. & Garikipati, S. Gender Inclusivity of India’s Digital Financial Revolution for Attainment of SDGs: Macro Achievements and the Micro Experiences of Targeted Initiatives. Eur J Dev Res 35, 1369-1391 (2023). |

| [13] | Vidani, J. (2024). A study on the rise and recent development in unified payments interface. SSRN Electronic Journal. |

| [14] | Santiso C. Govtech against corruption: What are the integrity dividends of government digitalization? Data & Policy. 2022; 4: e39. |

| [15] | Buteau, S., Rao, P. & Valenti, F. Emerging insights from digital solutions in financial inclusion. CSIT 9, 105-114 (2021). |

| [16] | Nayak Kini A and Basri S. An empirical examination of customer advocacy influenced by engagement behaviour and predispositions of FinTech customers in India [version 2; peer review: 2 approved]. F1000Research 2022, 11: 27 |

| [17] | Windasari, N. Kusumawati, N. Larasati, R. P. Amelia Digital-only banking experience: Insights from gen Y and gen Z Journal of Innovation & Knowledge, 7(2) (2022), Article 100170, |

| [18] | Pandey, S. K. (2022). A Study on Digital Payments System & Consumer Perception: An Empirical Survey. Journal of Positive School Psychology, 6(3), 10121-10131. |

| [19] | Hanedar, E., Alonso, C., Uña, G., Prihardini, D., Bhojwani, T., & Zhabska, K. (2023). Stacking up the Benefits: Lessons from India’s Digital Journey. IMF Working Paper, 2023(078), 1. |

| [20] | Gochwal, R. (2017). Unified payment interface—an advancement in payment systems. American Journal of Industrial and Business Management, 7(10), 1174-1191. |

| [21] | Ansar, M., Asif, N., & Mahale, P. (2024). The impact of unified payment interface (UPI) on financial inclusion and economic development: A digital innovation perspective. International Journal of Multidisciplinary Research and Growth Evaluation, 5(4), 452-457. |

| [22] | Inc42. The UPI Effect: How UPI Is Reshaping India’s Payment Industry. 2023 May 25. |

| [23] |

Chopra, C., & Gupta, P. (2023, June 26). India’s digital leap: the Unified Payment Interface’s unprecedented impact on the financial landscape. World Economic Forum.

https://www.weforum.org/stories/2023/06/india-unified-payment-interface-impact/ |

| [24] | Srivastava, N. (2019). Digital Financial Services: Challenges and prospects for liberalized and globalized Indian economy. SSRN Electronic Journal. |

| [25] | Fernandes, D., Lynch, J. G., Jr., & Netemeyer, R. G. (2014). Financial literacy, financial education, and downstream financial behaviors. Management Science, 60(8), 1861-1883. |

| [26] | Rastogi, S., Panse, C., Sharma, A., & Bhimavarapu, V. M. (2023). Unified Payment Interface (UPI): A Digital Innovation and Its Impact on Financial Inclusion and Economic Development. Journal of Digital Finance, 8(1), 45-62. |

| [27] | C. Paramasivan, and V. Ganeshkumar. “Overview of Financial Inclusion in India”. International Journal of Management and Development Studies, vol. 2, no. 3, Mar. 2013, pp. 45-49, |

| [28] | Vashisht, A., & Wadhwa, B. (2013). Financial inclusion - a tool to uplift people at ‘Bottom of Pyramid’ (BOP). SSRN Electronic Journal. |

| [29] | Dr. J. SureshKumar | Dr. D. Shobana "Exploring Digital Payments, Financial Inclusion, and Monetary Policy in India" Published in International Journal of Trend in Scientific Researchand Development (ijtsrd), ISSN:2456-6470, Volume-8 | Issue-1, February 2024, pp. 417-424, URL: |

| [30] | Rangrajan. (2008). Report on the committee of financial inclusion. http://slbckarnataka.com/UserFiles/slbc/Full%20Report.pdf Retrieved 8/2/2022 |

| [31] | Ambarkhane, D., Shekhar Singh, A. S., & Venkataramani, B. (2016). Developing a comprehensive financial inclusion index. Management and Labour Studies, 41(3), 216-235. |

| [32] | Sarma, M. (2008). Index of financial inclusion (Working Paper No. 215). New Delhi: Indian Council For Research On International Economic Relations. |

| [33] | Muharsito, M., & Muharam, H. (2023). The effect of digital financial inclusion on bank efficiency. INTERNATIONAL CONFERENCE ON RESEARCH AND DEVELOPMENT (ICORAD), 2(1), 1-6. |

| [34] | Singh, V., & Pushkar, B. (2019). A study on Financial inclusion: Need and challenges in India. SSRN Electronic Journal. |

| [35] | Reddy, C. V. (2016). 12 Pillars’ Framework for Successful Financial Inclusion in India. Indian Journal of Finance, 10(12), 7-28. |

| [36] |

BCG (2016). Digital Payment 2020.

http://image-srcbcg.com/BCG_COM/BCG-Google%20Digital%20Payments%202020-July%202016_tcm21-39245.pdf |

| [37] | Bhatia, A. Kumar, S. And Agarwal, A. (2016). A contemporary Study of Microfinance: A study for India’s Underprivileged. IOSR journal of Economics and Finance. pp. 23-31 |

| [38] | Rastogi, S., Panse, C., Sharma, A., & Bhimavarapu, V. M. (2021). Unified Payment Interface (UPI): A digital innovation and its impact on financial inclusion and economic development. Universal Journal of Accounting and Finance, 9(3), 518-530. |

| [39] | Sharma, A., Bhimavarapu, V. M., Kanoujiya, J., Rastogi, S., & Barge, P. B. (2022). Financial Inclusion - An Impetus to the Digitalization of Payment Services (UPI) in India. Journal of Asian Finance, Economics and Business, 9(9). |

| [40] | Ragini, B., & Prakash, J. V. (2024). Does unified Payment Interface (UPI) contribute to financial inclusion? The case of construction workers in Andhra Pradesh. In Springer proceedings in business and economics (pp. 257-272). |

| [41] | Serrao, M. V., Sequeira, A. H., & Hans, B. (2012). Designing a methodology to investigate accessibility and impact of financial inclusion. SSRN Electronic Journal. |

| [42] | Smith, B. (2025). A Novel Digital Payment Architecture: A Unified Payment Interface and its Systematic Transformation of Financial Infrastructure. Preprints. |

| [43] | Kamal, M., Rahmani, S., & Alam, M. R. (2025). Beyond Traditional Banking: How Fintech is Reshaping Financial Access in India. SSRN Electronic Journal. |

| [44] | Ambali, N., & Jaisingh, M. (2021). Impact of Unified Payment Interface on the Indian Banking System and Financial Inclusion. |

| [45] | Chaturvedi, R., & Sharma, S. (2021). Role of Unified Payments Interface (UPI) in Financial Inclusion of Rural India: An Analysis. |

| [46] | Baliyan, D., Singh, N., Faculty of Commerce, Hindu College, Moradabad, Uttar Pradesh, India, & Faculty of Commerce, Govt. Degree College, Punwarka, Saharanpur, Uttar Pradesh, India. (2023). UNIFIED PAYMENTS INTERFACE (UPI): A DIGITAL TRANSFORMATION IN INDIA. International Journal of Creative Research Thoughts (IJCRT), 11(3), g414. |

| [47] | VTK, S., Kulkarni, P., Justin, M. S. M., & Bhatta, N. (2023). Impact of UPI Utilisation on Financial Inclusion: Empirical Evidence from India. Journal of Management and Entrepreneurship, 17-17(1), 105-112. |

| [48] | Odedra K, Rabadiya B, Vidani J. An analysis of identifying the business opportunity in agro and chemical sector - with special reference to African country Uganda. Compendium of Research Papers of National Conference 2018 on Leadership, Governance and Strategic Management: Key to Success. Pune: DY Patil University Press; 2018. p. 96-100. |

| [49] | Vidani, J. (2024b). A study on the rise and recent development in unified payments interface. SSRN Electronic Journal. |

| [50] | Chaudhari, A., & Chaudhari, D. (2019). To Study the Consumer Satisfaction on UPI (Unified Payments Interface) with Special Reference to Hyderabad and Suburbs. Research Journey‟ International Multidisciplinary E-Research Journal. |

| [51] | Garg, P., & Panchal, M. (2017). Study on Introduction of Cashless Economy in India 2016: Benefits & Challenge’s. IOSR Journal of Business and Management, 19(04), 116-120. |

| [52] | PIB. (2023, 12 27). Ministry of Finance Year Ender 2023: Department of Financial Services. Retrieved from PIB: |

| [53] | Gaurav Agrawal, P. J. (2019). Digital Financial Inclusion in India: A Review. Behavioral Finance and Decision Making Models, 9. |

APA Style

Sharma, K. (2025). Evaluating UPI's Role in Advancing Financial Inclusion and MSMEs' Development in India. International Journal of Economics, Finance and Management Sciences, 13(5), 336-344. https://doi.org/10.11648/j.ijefm.20251305.19

ACS Style

Sharma, K. Evaluating UPI's Role in Advancing Financial Inclusion and MSMEs' Development in India. Int. J. Econ. Finance Manag. Sci. 2025, 13(5), 336-344. doi: 10.11648/j.ijefm.20251305.19

@article{10.11648/j.ijefm.20251305.19,

author = {Kanak Sharma},

title = {Evaluating UPI's Role in Advancing Financial Inclusion and MSMEs' Development in India

},

journal = {International Journal of Economics, Finance and Management Sciences},

volume = {13},

number = {5},

pages = {336-344},

doi = {10.11648/j.ijefm.20251305.19},

url = {https://doi.org/10.11648/j.ijefm.20251305.19},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ijefm.20251305.19},

abstract = {In 2016, the Indian government took a very firm stance on the black money market, which was followed by demonetization. Afterward, the government realized that the economy would benefit more from digital transactions and plastic money, considering Singapore as a reference. People were struggling to meet their basic needs; consequently, the government understood the importance of stabilizing the money supply, leading to the emergence of digital transactions and UPI. Objective: to investigate the dynamics of UPI transactions post-2020 and how UPI has been very critical in making financial inclusion a possibility in the Indian scenario. The paper also evaluates the role of UPI in MSMEs growth and development. Methods: Information about UPI transactions, including their volume and value, the number of active users, and their geographic distribution, was gathered using the NPCI dataset, on which we ran a linear regression model. For MSMEs, we saw a span of the last 4 years through the government’s annual report. Findings: Linear regression showed time predicts UPI transaction volume (R² = 0.97, p < 0.001) and value (R² = 0.837, p < 0.001), indicating that UPI adoption growth explains much of the rise in digital activity. The compound annual growth rate of UPI transaction value was about 19.75% from 2020 to 2024. The MSME transaction data from 2020-21 to 2023-24 shows a trend of an increase in the number and value of transactions, with the vast majority of them being carried out online during this time.

},

year = {2025}

}

TY - JOUR T1 - Evaluating UPI's Role in Advancing Financial Inclusion and MSMEs' Development in India AU - Kanak Sharma Y1 - 2025/10/18 PY - 2025 N1 - https://doi.org/10.11648/j.ijefm.20251305.19 DO - 10.11648/j.ijefm.20251305.19 T2 - International Journal of Economics, Finance and Management Sciences JF - International Journal of Economics, Finance and Management Sciences JO - International Journal of Economics, Finance and Management Sciences SP - 336 EP - 344 PB - Science Publishing Group SN - 2326-9561 UR - https://doi.org/10.11648/j.ijefm.20251305.19 AB - In 2016, the Indian government took a very firm stance on the black money market, which was followed by demonetization. Afterward, the government realized that the economy would benefit more from digital transactions and plastic money, considering Singapore as a reference. People were struggling to meet their basic needs; consequently, the government understood the importance of stabilizing the money supply, leading to the emergence of digital transactions and UPI. Objective: to investigate the dynamics of UPI transactions post-2020 and how UPI has been very critical in making financial inclusion a possibility in the Indian scenario. The paper also evaluates the role of UPI in MSMEs growth and development. Methods: Information about UPI transactions, including their volume and value, the number of active users, and their geographic distribution, was gathered using the NPCI dataset, on which we ran a linear regression model. For MSMEs, we saw a span of the last 4 years through the government’s annual report. Findings: Linear regression showed time predicts UPI transaction volume (R² = 0.97, p < 0.001) and value (R² = 0.837, p < 0.001), indicating that UPI adoption growth explains much of the rise in digital activity. The compound annual growth rate of UPI transaction value was about 19.75% from 2020 to 2024. The MSME transaction data from 2020-21 to 2023-24 shows a trend of an increase in the number and value of transactions, with the vast majority of them being carried out online during this time. VL - 13 IS - 5 ER -

Department of Economics, University of Delhi, New Delhi, India